The 10-Year Treasury: It’s Less Than You Think

When the Fed was created in 1914, it was set to task of controlling short-term interest rates in an attempt to iron out financial cycles.

When the Fed was created in 1914, it was set to task of controlling short-term interest rates in an attempt to iron out financial cycles.

It succeeded for many years. But by avoiding the natural rebalancing (and occasional pain) from free markets, we just got a bigger bubble into 1929.

Then, when it finally burst, we got the greatest depression in all of modern history!

Since the Fed and other central banks were created, they have always manipulated short-term interest rates to try to encourage borrowing and spending in slowdowns – to make the natural economic cycle “go away.”

And every time, it suppresses the economic cycles that were already in place, until finally they come roaring back.

So it always strikes me as funny to see highly educated, seemingly reasonable people in pin-striped suits and pantsuits stand in front of us and basically say that there’s a free lunch after all – that we can get something for nothing!

To them, economics is no longer a matter of supply and demand, free markets and rebalancing. They think we’ve found a way to program the economy so we never have a recession again.

If someone sold you instant pain relief in an infomercial, you’d probably buy it…

But if someone stood on the streets and babbled such nonsense, you’d call them delusional or even psychotic – snake oil salesmen.

All the apparent education and sophistication of these top economists, financial officials and central bankers boils down to this simple automaton explanation: if we don’t keep taking more of the financial drug that we used to keep the bubble going, like zero interest rates and QE, we will collapse and go into detox.

It’s the same logic of any extreme addict. When a serious drug addict comes off a high, he realizes the only non-painful choice is to take more of the drug.

As Charlie Sheen said: “the key to drinking is to not stop.”

My interpretation: you don’t get something for nothing, and by going into denial and doing things that make you feel better today while ignoring the consequences, you simply make the inevitable comedown worse.

And that’s exactly what central banks have done today. They’ve always meddled with short-term interest rates. But outside of emergency times like in World War II, they have never substantially printed money to buy their own bonds to suppress longer-term interest rates as well.

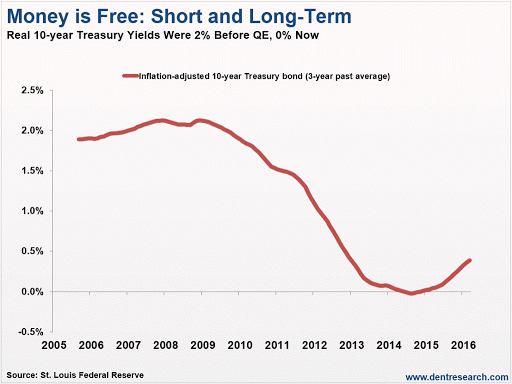

Look at this chart that shows the 10-year, risk-free Treasury bond rate. Today, it stands around 1.79%. When adjusted for three-year average inflation rates, it’s much lower:

After years of non-stop QE, its yields had actually fallen to 0% in late 2014, and today it’s still only around 0.4% – practically zero!

Most people don’t understand that all other financial assets are heavily influenced by the 10-Year Treasury bond rate (or similar sovereign bonds in other countries).

Higher-risk bonds from AAA corporate to junk are valued as a risk premium for default above the risk-free rate. Lower risk-free rates mean lower bond yields and higher bond values all the way up the junk bond scale.

Loans for mortgages and auto loans, etc. go down in rates, with a risk premium that is very low on government guaranteed mortgages. That makes real estate and other highly financed assets more valuable, as everyone can buy more for the same monthly payment.

Lower rates mean higher stock values as well. Stocks are basically valued by projecting earnings 10 years out, and then discounting their value to the present by adjusting for the interest on the 10-year, risk-free rate.

At lower long-term rates, companies can borrow at near zero adjusted for inflation, and buy back their own stocks to increase earnings per share – even if earnings are not growing. Or, they can buy out or merge with a company financed by cheap debt… the list goes on.

It’s all about financial engineering – not about productive investment in future assets and employment.

This final bubble since early 2009 is a total illusion from QE and financial engineering – not the normal fundamentals of rising demographics, innovation and productivity, like 1983 to 2007.

And as an illusion, it will disappear much faster than it was created when it finally bursts. Now you see it… now you don’t.

Note: The author of this article is Harry Dent.

Category: What's Going On?