5 Funds That Could Double Your Retirement Nest Egg

If you want to save a million dollars, you need to save a ton of money over a lifetime. Or at least that’s what we’re constantly told.

If you want to save a million dollars, you need to save a ton of money over a lifetime. Or at least that’s what we’re constantly told.

But it’s not true.

The fact is, you can save $1 million a lot quicker by saving just $298 per month. It just takes a contrarian’s view on the markets and the confidence to invest differently than the herd.

In a moment, I’ll give you 5 fund picks to start you off on the right foot.

First, let’s look at the math.

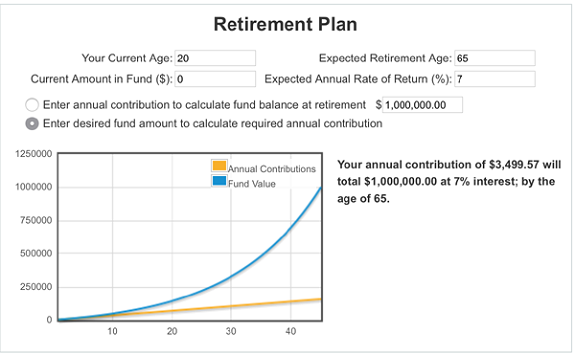

Any retirement calculator, like the one below from Bloomberg, can calculate how much money you need to contribute to your retirement fund to reach your goal. If we want to save a million bucks starting with nothing, we have two choices. Either we can wait nearly half a century…

The Slow Boat to Financial Freedom

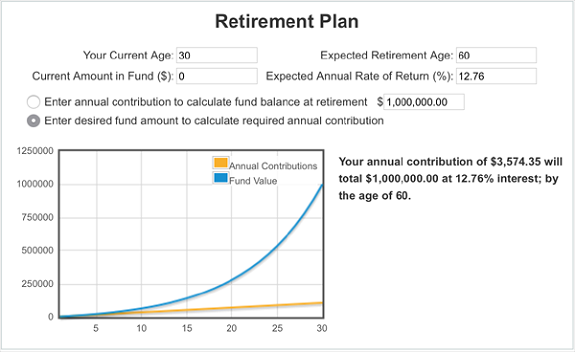

…or we can become millionaires faster if we can get a better return.

A Shortcut to 7 Figures

Most financial advisors will tell you to expect a 7% average annual return over the long term on a diversified portfolio of stocks and bonds. And they’re right; most conventional financial wisdom will steer you to a portfolio of US stocks and US Treasuries that will have historically returned something close to that.

But if you can get the 12.8% average annual return you see above, you can become a millionaire much faster—in just 30 years, as opposed to 45.

I know. That’s a big “if,” right?

Not really. Let me show you a basket of assets that have provided that return over the last decade.

You might think you can only get 13% if you concentrate your investments in ultra high-risk, highly volatile bets that are more likely to fail than succeed. But that’s just not the case. The truth is, this kind of return is possible with a combination of plain-vanilla stocks, corporate bonds and municipal bonds.

Yes, munis—one of the safest and least volatile asset classes on Earth.

Here’s how you do it.

First, we’ll buy stocks through the Nuveen NASDAQ 100 Dynamic Overwrite Fund (QQQX), which uses a covered-call strategy to get income on its tech stock portfolio. Thanks to the volatility of the tech industry, the income from these call options is very high, helping the fund return 150% over the last decade.

And that’s one of our portfolio’s worst performers.

On top of that, we’ll add the Deutsche Municipal Income Trust (KTF), a diversified municipal bond fund that’s been around since the 1980s.

Then we’ll add the PIMCO Corporate & Income Opportunity Fund (PTY), the Flaherty & Crumrine Preferred Securities Income Fund (FFC) and Main Street Capital Corporation (MAIN). This gives us preferred stocks, corporate bonds and municipal bonds, as well as a business development company that’s easily the best in its class, investing in high-quality small- and medium-sized firms across the country.

Now let’s look at how these stocks did over the last decade.

Crushing the S&P 500

On average, we’re getting a 232% return on our investment over the last decade—or an annualized 12.8% return. That’s much better than the 6.5% annualized return from the SPDR S&P 500 ETF (SPY) over the same period.

Retirement experts will tell you that you can comfortably withdraw 4% per year from a portfolio without worrying about running out of cash in retirement, so if we follow that advice, that $1 million would turn into a $40,000 passive income.

There’s only one hitch: these funds were great buys a year ago, but some of them now trade at premiums to their net asset values (NAV), which means they might not continue to offer these stellar returns.

If they fall short, you’d be looking at a smaller-than-expected nest egg—and a less-comfortable retirement.

This is why we developed our “No-Withdrawal” retirement portfolio. It lets you pocket that same $40,000 income stream in retirement, and you won’t need a cool million to do it.

In fact, you’ll need only half that much.

That’s because this portfolio throws off an 8.0% average yield, so you’re already locking down more half the 12.8% annualized return I mentioned above right out of the gate.

What does that mean for you? Simply this: no matter what happens with the markets, your income is safe, and you’ll never have to sell a single share to keep it coming. So you can forget about the flawed 4% withdrawal rule!

I can’t wait to show you the ins and outs of our strategy. Simply click here to get full details on our portfolio and discover the bargain-priced 8.0%+ yielders inside it.

Category: Closed-End Funds (CEFs)