How To Live Off $500,000 Forever

A half-million dollars is a lot of money. Unfortunately, it won’t generate much income today if you limit yourself to popular investments.

A half-million dollars is a lot of money. Unfortunately, it won’t generate much income today if you limit yourself to popular investments.

The 10-year Treasury has “rallied” to 1.85%. Put your $500K in them and you’re well below the single-person poverty level at $9,250 annually. Yikes.

Dividend paying stocks are masquerading around as bond proxies for this reason. But they still don’t yield enough. Vanguard’s popular Dividend Appreciation ETF (VIG) pays 2.1%. The iShares Select Dividend ETF (DVY) pays 3.2% – better, but that’s still just below the poverty level for two people at $16,000 per year.

When investment income falls short, retirees sell their investments to supplement the income. Of course the problem here is that when capital is sold, the payout stream takes an immediate hit – so that more capital must be sold next time, and so on.

The Only Reliable Retirement Solution: No Withdrawals

Rather than rely on, say, a 4% annual drawdown for income, the only dependable way to retire and stay retired is to boost your payouts so that you never have to touch your capital.

This is easier said than done, and obviously the more capital you have the better off you are. But with rates and yields so low, even rich guys have a tough time living off interest today.

You can actually live better than they can off a (much) more modest nest egg if you know where to look for lesser-known, meaningful and secure yield. I’m talking about annual income of 6%, 7% or even 8% – so that you’re banking up to $40,000 each year for every $500,000 you invest.

And you’ll never have to touch your nest egg capital – which means you’ll never have to worry about stock prices.

The only thing you need to concern yourself with is the security of your dividends. As long as your payouts are safe, who cares if your stock prices swing up or down on a given day?

Most investors know this is the right approach to retirement. Problem is, they don’t know how to find 7% and 8% yields to fund their lives.

And when they do find high yields, they’re not sure if these payouts are safe. Will the company or fund have enough cash flow to pay the dividends into the future? And how sensitive are these payouts to interest rate increases?

Let’s walk through my three favorite corners of the investment universe for income today – with a special focus on the interest rate question, which is mistakenly believed to be a high income threat by headline-focused investors.

“No Withdrawal” Play #1: Closed-End Funds

Some closed-end funds (CEFs) paying up 7%, 8% or even 9% can be good income candidates – if you choose wisely.

You’re probably familiar with their mutual “cousins”. Closed-ends are a bit different. While mutual funds tend to buy individual stocks and mirror the market, CEF managers tend to have wider mandates and longer leashes. A top CEF manager takes advantage of this flexibility to generate alpha.

He might buy safe sovereign debt in Australia when investors are scared of Asia altogether, and lock in secure 6% yields. Or he might buy preferred shares issued by JPMorgan paying 6.1% annually – a deal not available to an individual investor like you or me (more on this in a minute).

A savvy closed-end manager can even borrow cheaply and juice returns. CEFs borrow at rates tied to Libor (the London interbank offered rate) – good living today with the international benchmark at just 0.86%. The “spread” turns already good yields into great ones.

With a Fed rate hike likely next month, closed-ends are being tossed out with other high-income investments that “should” be hurt with rising rates. Too bad for the investors who are selling, because their assumptions are lazy, and wrong!

How do you think CEF’s performed from June 30, 2004 to June 30, 2006 when Fed chair Alan Greenspan increased the federal funds rate from 1% to 5.25%?

They did great. In fact, three prominent funds – the Gabelli Dividend & Income Trust Fund’s (GDV), the Calamos Strategic Total Return (CSQ) and the Eaton Vance Limited Duration Income Fund (EVV) – all outperformed the market during this 2-year span!

Higher Rates No Problem for Top Closed-Ends 2004-06

“No Withdrawal” Play #2: Preferred Shares

You can double your yields, and actually reduce your risk, by trading in your common shares for preferreds. Most investors only consider “common” shares of stock when they look for income. These are the shares in a company you receive when you place an order with your broker.

Problem is, most dividend darlings don’t pay much on their common shares today. You’ll be hard pressed to find a dividend aristocrat with a yield above 3% or a P/E ratio below 20 – evaporating business models or not!

A Bear Market in Common Yields

A company will issue preferred shares to raise capital. In return it will pay regular dividends on these shares – and as their name suggests, preferreds do receive their payouts before common shares. They typically get paid more, and even have a priority claim on the company’s earnings and assets in case something bad happens, like bankruptcy.

So far so good. The tradeoff? Less upside. But in today’s expensive stock market, it may not be a bad trade to make. Here’s an example that would roughly double your current dividends.

Common shares of JPMorgan (JPM) – which I like and own warrants on – pay 2.9%. Not bad, but you could more than double your yield by buying JPM’s “Series Y” preferred stock offering for 6.1% annually.

Series what? That’s a big problem with preferred shares – they are often complicated to purchase without the help of a human broker.

I’ll show you how to purchase my favorite preferred funds for 7.8% and 8% yields in a minute. The best management teams buy mostly floating rate bonds – which will buffer their portfolios as interest rates rise. It’s important to stick with the experts and avoid convenient ETFs, which aren’t “smart” enough to do this.

“No Withdrawal” Play #3: Recession-Proof REITs

Real estate investment trusts, or REITs, can be powerful investment vehicles for safety and high yield. Legally required to return 90% of income to shareholders, these firms find high-quality real estate opportunities while providing investors to opportunity to be a landlord with the liquidity – and convenience – of a stock.

Some REITs are relatively recession-proof. While REITs that specialize in strip malls or hotels suffer if a recession hits, others such as healthcare REITs will see steady demand no matter what happens with the broader economy. Sector staple Ventas (VTR) pays 3.9% today, and some quality issues actually pay 7% or 8% or better.

Meanwhile self-storage REITs like Public Storage (PSA) can actually see an uptick in demand when economic trouble strikes. For example, in 2008 when millions of Americans were losing their homes, demand for self-storage went up as people abandoned their underwater houses and looked for a place to keep their valuable possessions.

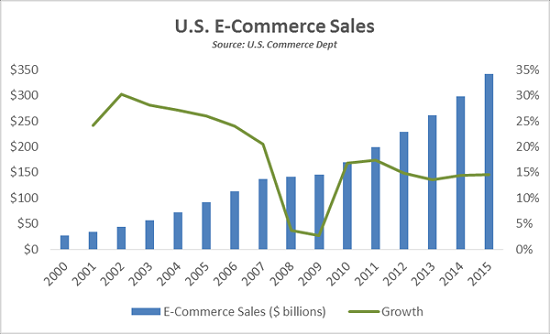

PSA only pays 3% today, but Stag Industrial (STAG) yields 5.6%. It owns, operates and rents 290 standalone industrial buildings, most of which are warehouses or distribution centers in hot demand thanks to the e-commerce megatrend.

E-Commerce Sales Booming in America

The financial talking heads claim that REIT profits will be crushed as rates rise. It sounds reasonable enough, because these firms do benefit from cheap borrowing. However it’s a lazy explanation, and not actually true for many REITs over any meaningful time period.

Let’s go back to the 2004-06 period in which Greenspan hiked. He boosted the federal funds rate from 1% to 5.25% while the 10-year Treasury glided higher from 4.5% to 5.15%.

Terrible time for REITs, right? Wrong. The Vanguard REIT ETF (VNQ) actually returned 48.1% including dividends over this time period, crushing the 14.6% gain by the S&P 500:

REITs Crushed Other Stocks as Rates Rose

Last year at this time, we were having the same conversation we are right now. REITs were supposedly “done” because the Fed was about to raise rates in December. The hike happened, but REITs still beat the broader stock market over the ensuing 12 months:

REITs Brushed Off The Last Hike

My Two Favorite Preferred Funds Pay 7.8% and 8% Today

Now let’s talk about two great income buys you can make today, which combine the best aspects of two of the strategies I described.

Now the complexity of buying preferred funds tempts many investors to streamline their online buys and simply purchase ETFs like the PowerShares Preferred Portfolio (PGX) and the iShares S&P U.S. Preferred Stock Index Fund (PFF). After all these funds pay 5.7% each and, in theory, they diversify your credit risk.

Be careful because I believe they actually expose you to unnecessary credit risk. The only way you lose with this vehicle is by giving your money to a driver who crashes your car. But the S&P 500 and NASDAQ are large enough that there’s usually a company financially crashing into a brick wall at any moment in time.

And if we include the brick wall the financial world ran into ten years ago, these funds haven’t even performed to their current yields:

The Problem With Financial Brick Walls

I suspect PGX and PFF probably won’t actually return 5.7% annually over the next decade, either. Which why I recommend moving past a broad-based ETF in favor of a fund with an active manager working for you. There’s extra yield to be had in preferred shares – but you should make sure you have an expert buying your stock to keep you safe and on the road.

My two favorite preferred share funds pay 7.8% and 8% respectively. They’re excellent bargains because they are closed-end funds selling at discounts to their net asset values (NAVs).

Earlier this year, investors irrationally sold any and all closed-ends down to silly bargain prices. Some deservedly so, but these two high quality preferred funds – with excellent management teams and track records – were swept away by the hysteria.

That’s great for us. Low prices mean higher yields plus some upside as these funds gradually close their discount windows. And these 7.8% and 8% yields net us 37% more income, and do so more securely, than their ETF counterparts. Plus, these funds have a history of actually delivering these types of returns over the long haul (unlike the more popular ETFs).

Lesser-known high-income plays like these are the cornerstones of my “no withdrawal” retirement portfolio strategy.

That’s why, in today’s low yield world, I specialize in finding safe and under-the-radar high-income options. Click here and I’ll explain more about my no withdrawal approach – plus I’ll share the names, tickers and buy prices of my two favorite preferred funds for 7.8% and 8% yields.

Category: What's Going On?