A Simple All-ETF Portfolio That Pays 4.3%

The stock market is complicated and volatile. This is why professional investors diversify their investments into a large batch of stocks. But buying many different companies is not easy—the more you diversify, the more research you need to do to make sure you aren’t buying a dud.

The stock market is complicated and volatile. This is why professional investors diversify their investments into a large batch of stocks. But buying many different companies is not easy—the more you diversify, the more research you need to do to make sure you aren’t buying a dud.

This is why ETFs have become incredibly popular. They give investors the opportunity to buy a basket of stocks in a single market sector or asset class. But now there are thousands of ETFs out there, and some of them come with hefty fees and poor performance. For good returns, we should avoid these dogs.

So where can we go instead for diversification and yield? With this 5-fund portfolio, and you can net dividends over 4% with some of the lowest management fees in the ETF universe:

A Diversified, Low-Cost & High Yield ETF Portfolio

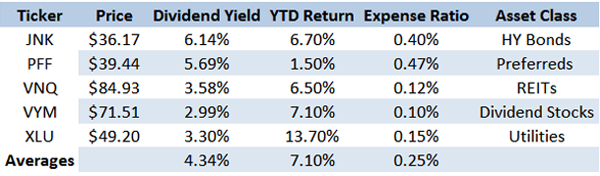

What’s in the fund? Let’s start with the SPDR Barclays High Yield Bond fund (JNK), a collection of high yield corporate bonds that offer investors a highly diversified income stream. The fund is incredibly cheap—with an expense ratio of 0.40%, you’re paying just $4 for every $1,000 invested. Plus, this fund is easy to trade, with millions of shares trading every day.

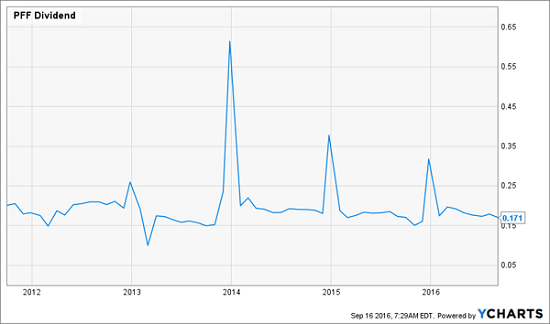

Next is the iShares U.S. Preferred Stock Index Fund (PFF), with an impressive 5.7% dividend and a similarly diversified portfolio of hundreds of preferred stocks. This fund’s expense ratio is the highest of the batch, at 0.47%—but that’s still minuscule compared to many other funds out there. Plus, the fund also pays special dividends that can significantly boost your income:

Heartbeats to Wealth

This “heartbeat” chart shows the sudden beeps of big payouts to ETF holders, which vary greatly from one year to the next depending on how well preferred stocks are doing. There is of course the problem that dividends are pretty flat—so let’s add a fund that gives us growing payouts.

The Vanguard REIT Index ETF (VNQ) fits that bill. I’ve written recently about how I love REITs, and with good reason—VNQ is up 6.5% year-to-date on top of its 3.6% dividend yield. That’s a double-digit return, and we aren’t even to the end of 2016 yet.

Another thing I like about VNQ is that its total return, including dividends, is actually below its average over the last 5 years despite the fact that REITs are up big in 2016:

VNQ Still Has Room to Rise

Vanguard makes another appearance in our ETF portfolio with the Vanguard High Dividend Yield Index (VYM). I like Vanguard for their amazingly low management fees (a 0.10% expense ratio is almost nothing) as well as their historical returns. VYM is also really cheap right now, with a P/E ratio of 20.7 versus the 24.8 P/E ratio for the broader S&P 500. Plus its dividend yield, at 3%, is almost 50% higher than the S&P 500. One more benefit to VYM – its dividends are growing fast:

Rising Payouts for VYM Shareholders

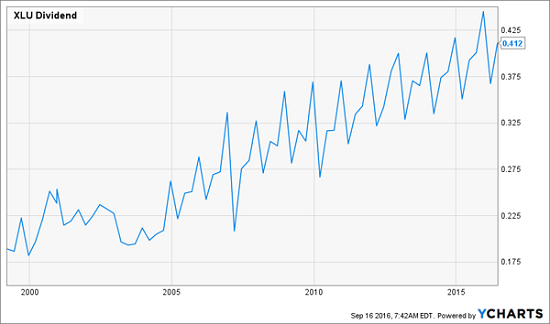

Finally let’s look at the SPDR Utilities Select Sector fund (XLU). XLU is up 13.7% year-to-date as investors rediscover these boring but lucrative stocks. Tack on a 3.3% dividend yield, and you’ve got a massive return on your investment with this one fund.

The other good thing about XLU: its companies raise their dividends annually.

More Income for XLU Holders

The longer you hold XLU, the more dividend income you’ll get. Plus, XLU’s price is up 45% over the last 5 years. With capital gains and a rising stream of high income, what’s not to like?

Of course, this all-ETF portfolio is easy, but it’s far from ideal. I’ve written in the past about the problems with a fund like JNK, but the short version is this: junk bonds carry the downside of lower oil prices, without the upside of a straight bet on oil. Fortunately, oil doesn’t seem to be tanking anytime soon which makes this fund a bit better than when I wrote back in January, but it’s still not perfect.

Then there’s PFF. What’s wrong with this fund? As I wrote last week, these funds expose investors to unnecessary credit risk, meaning its dividend payout is unlikely to grow any more in the future than it has in the past.

These ETFs aren’t perfect, but they are easy. An investor can pour $1 million into these funds and get an income stream of $43,400 per year. But there is a better way. There are cheaper, higher paying funds that retirees can use to create a dividend portfolio that provides a high level of current income while also protecting from major market downsides.

Plus, you don’t need $1 million to get that $43,400 income stream. In fact, I can show you funds better than JNK and PFF that will get you that same amount of income with in investment of just $543,000 – only half the capital thanks to double the yields!

I call it the “No Withdrawal” Retirement Portfolio, and it is designed to provide investors with a steady 8% income stream while keeping their capital safe from the increasingly volatile stock market. Click here and I’ll show you the three “no withdrawal” stealth plays I use to bag 8% yields so that I can actually fund my retirement on dividends alone.

Category: Dividend ETFs