Why Interest Rates Are Low (Hint It’s Not The Fed)

After dominating investment news headlines on a regular basis over the past 15 years, the Federal Reserve has found its way into the middle of the presidential election. Donald Trump has accused the Fed of propping up a “false economy” and argued that “the rates are going to have to change.” Hillary Clinton hit back by arguing that Trump should not be commenting on the Fed’s actions while running for president.

After dominating investment news headlines on a regular basis over the past 15 years, the Federal Reserve has found its way into the middle of the presidential election. Donald Trump has accused the Fed of propping up a “false economy” and argued that “the rates are going to have to change.” Hillary Clinton hit back by arguing that Trump should not be commenting on the Fed’s actions while running for president.

Since then, various pundits have debated the merits of each candidate’s case. Ultimately, though, the particulars of their arguments are irrelevant. Endlessly debating the actions of the Fed, either by political candidates or financial talking heads, has become a sideshow that distracts from the real workings of the economy and the stock market.

It’s time to consider a new paradigm for interest rates – a paradigm where treasury rates remain ultra low and riskier investments are priced by a decentralized market instead of a central bank.

For years, we have been warned that interest rates will inevitably rise from their “artificially” low levels back to the “normal” levels of the early 2000’s.

In the mainstream narrative, the Fed has been artificially holding interest rates down to stimulate the economy, and soon it will have to raise rates to more normal levels. If it fails to do so, pundits warn, the economy could suffer dire consequences.

There are three problems with this narrative:

- Today’s low rates represent the long-run natural cost of capital.

- Perpetually low interest rates can have positive effects on the economy.

- The Fed doesn’t control interest rates, the market does.

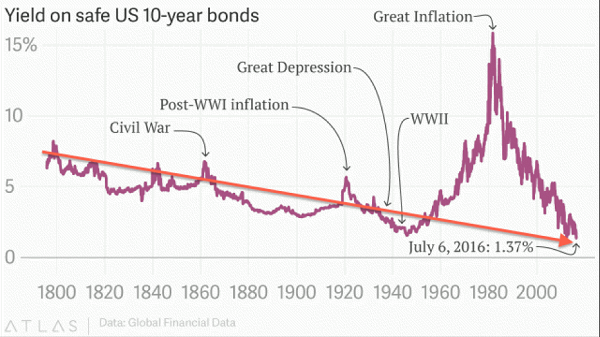

Lower Rates Fit Long-Term Trend

Figure 1: Long-Term Decline In Interest Rates

Sources: Quartz and New Constructs, LLC

Most analysts predicting a return to higher interest rates cite the past several decades as evidence that a higher cost of capital is the norm. Figure 1 shows the long-term trend in interest rates suggests otherwise. If we treat the massive spike in the late 20th century as an aberration, today’s low interest rates look like the continuation of a 200+ year trend.

It’s not just the Fed that’s been holding rates down for the past several years. It’s been structural shifts to the economy such as low inflation expectations, an aging population (more savers, fewer workers), increasing economic stability, and a variety of other factors recently detailed in the Wall Street Journal.

Not all fixed income securities will have low rates. We are saying that the floor on rates should remain low, and that the Fed would be well advised to recognize this shift as a new paradigm.

What This Means For Investors – Big Picture

For years, the investing public has pored over the minutes of every Fed meeting searching for clues as to when rates will rise. Countless articles have been written advising investors on ways to set up their portfolios to benefit from rising rates.

We recommend investors spend less time watching the Fed and trying to anticipate macro-driven stock market movements. Instead, investors should get back to the basics of real fundamental research on individual stocks. Success in markets today, and going forward, will be more about identifying mis-priced securities than riding general market movements up or down.

For example, many highly profitable companies with great upside have been significantly undervalued due to the market’s obsession over the Fed’s activities and the mistaken assumption that interest rates are destined to rise.

What This Means For Investors – Long idea

Mortgage REITs represent one area with some compelling value opportunities. Many of these stocks have depressed valuations due to concerns that rising rates would increase their cost of capital, decrease mortgage activity, lead to higher rates of default, and decrease their attractiveness to yield-seeking investors.

Redwood Trust (RWT) is one of our favorite stocks in the Mortgage REIT sector and earns our Very Attractive rating. RWT has generated over $200 million in free cash flow (19% of its market cap) over the trailing twelve months. Rising debt on the balance sheet may seem like a red flag to some investors, but this is merely the result of RWT cutting back on its off-balance sheet debt. The company’s total indebtedness actually declined over the past year.

At its current valuation of ~$14/share, RWT has a price to economic book value (PEBV) of just 0.7, which implies the market expects a permanent 30% decline in after-tax profit (NOPAT). The market is pricing in a decline from rising interest rates. If those rising rates don’t materialize, RWT promises significant upside with an 8% dividend yield.

What This Means For Investors – Sell Warning

On the other hand, investors should expect rising rates to bail out certain struggling companies, including many large insurers. Low rates make it difficult for insurers to earn high returns due to the fact that they are required to hold a significant amount of safe debt to guarantee they can cover the insurance policies they write.

American International Group (AIG) is one of our least favorite insurers and earns our Dangerous rating. AIG’s after-tax profit (NOPAT) has declined steadily since 2013 and turned negative over the trailing twelve months. Management has made a priority of selling non-core assets to return capital to shareholders, but the company’s prospects for sustainable long-term profit growth in a low-rate environment look increasingly bleak.

To justify its current valuation of ~$59/share, AIG would need to grow NOPAT from 2015 levels by 6% compounded annually for 20 years. In the new normal of low rates, AIG will struggle to achieve sustainable growth at such a level.

Do Your Own Diligence

Investors shouldn’t make decisions by listening to political rhetoric or talking heads. Success in investing comes from diligent research to understand a company’s true cash flows and the market’s expectations for future cash flows. Time to get back to the basics of securities analysis.

Note: The author of this article is David Trainer. He is a contributor to ValueWalk.com.

Category: What's Going On?