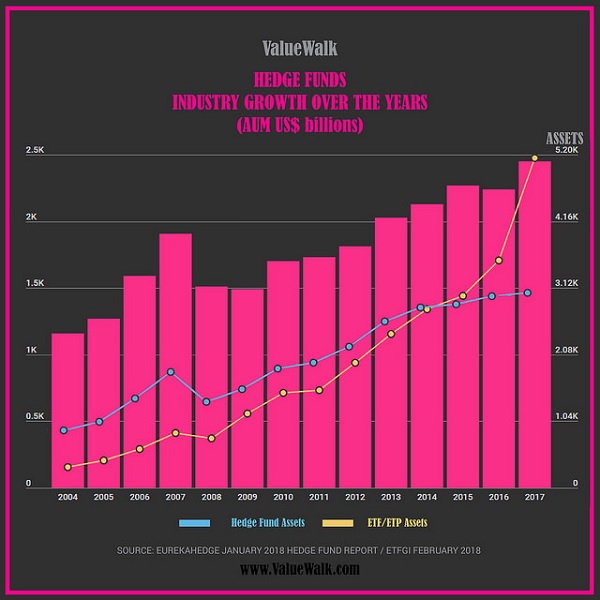

Media’s Misunderstanding Of ETFs

Every time the market has a period of extreme volatility, as it did in early February, there is no shortage of TV personalities who find a way to blame it on the ETF industry.

Despite the fact that the ETF industry has done more good for the average investor in terms of lowering fees, providing transparency and helping investors build intelligent portfolios than any other development in the industry in the last 50 years, their success sometimes makes them an easy target.

I am not going to focus on the VelocityShares Daily Inverse VIX Short-Term ETN (XIV), the short-volatility ETN that Credit Suisse recently closed as the market value of the product fell more than 90%. For one thing, it is a debt instrument issued by a bank, not an ETF.

This is not an insignificant distinction, as banks can create notes on many things that the SEC would not approve as a fund; for example, bitcoin. And while XIV was seen as causing the volatility, my guess is that there were many short-volatility bets across many instruments being unwound as interest rates spiked, and XIV was just the most visible.

Bubble In Passive Investing?

The issue that caught my ear was talk about a “bubble” in passive investing caused by ETF investors. Truthfully, I really don’t even understand what that means.

Markets have historically traded at high valuations in certain times of animal spirits such as the Nifty Fifty in the 1970s or the internet stocks in the 1990s, and they will continue to do so from time to time.

As investors clamored to increase equity positions last year as the economy strengthened and the tax cut was becoming a reality, ETFs were the most efficient way to quickly put large amounts of capital to work. This is a benefit of the structure, not a fault.

So, is the bubble that TV pundits hint at in specific stocks because they are part of an index and must be bought as cash flows into new ETF creation units?

I concede that, all things equal, it is good for the valuation of certain individual stocks to be in an index. But I don’t concede that it is harming the markets in any way. If anything, it should be relatively easy for active managers to outperform indexes if certain constituents get temporarily overvalued when new cash floods into the market.

Index Rebalancing Key Factor

Another critical factor that is overlooked is that many ETFs are based on indexes that do indeed rebalance according to certain criteria, such as minimum volatility, dividends, earnings or a combination of factors.

These funds are really systematic active strategies. They just happen to be transparent and predictable; again, a benefit of the structure.

Finally, many portfolios these days are created by actively managing a series of underlying passive and smart-beta ETFs (as Astoria does).

For example, many investors are increasing international ETF allocations this year relative to the U.S. as valuations tend to be lower overseas—a rebalancing process exactly the opposite of creating a bubble.

Find A Scapegoat Elsewhere

In times of market stress, you can always find a pundit who will paint with a broad brush and cast blame on the ETF industry. Often it is from active managers who find it very difficult to compete against ETFs that have a series of fee, tax efficiency, transparency and flexibility features that they do not have.

The reality is that the ETF industry’s success has spawned many additional products that offer different exposures with different methodologies in different structures and with different tax treatment.

While it is important to have expertise in these areas to create optimal ETF portfolios, the industry is as sound as ever, and the pundits need to find a different scapegoat.

Best, Bruce Lavine,

Senior Strategy Advisor

Any ETF Holdings shown are for illustrative purposes only and are subject to change at any time. For full disclosure, please refer to our website: astoriaadvisors

Note: This article was originally published at ValueWalk.com.

Category: ETFs